- Nexan Insights

- Posts

- From Shadowy Intelligence to Open-Sourced Fortune

From Shadowy Intelligence to Open-Sourced Fortune

The Palantir Story Investors Need to Know

Ajit Banerjee

May 13, 2025

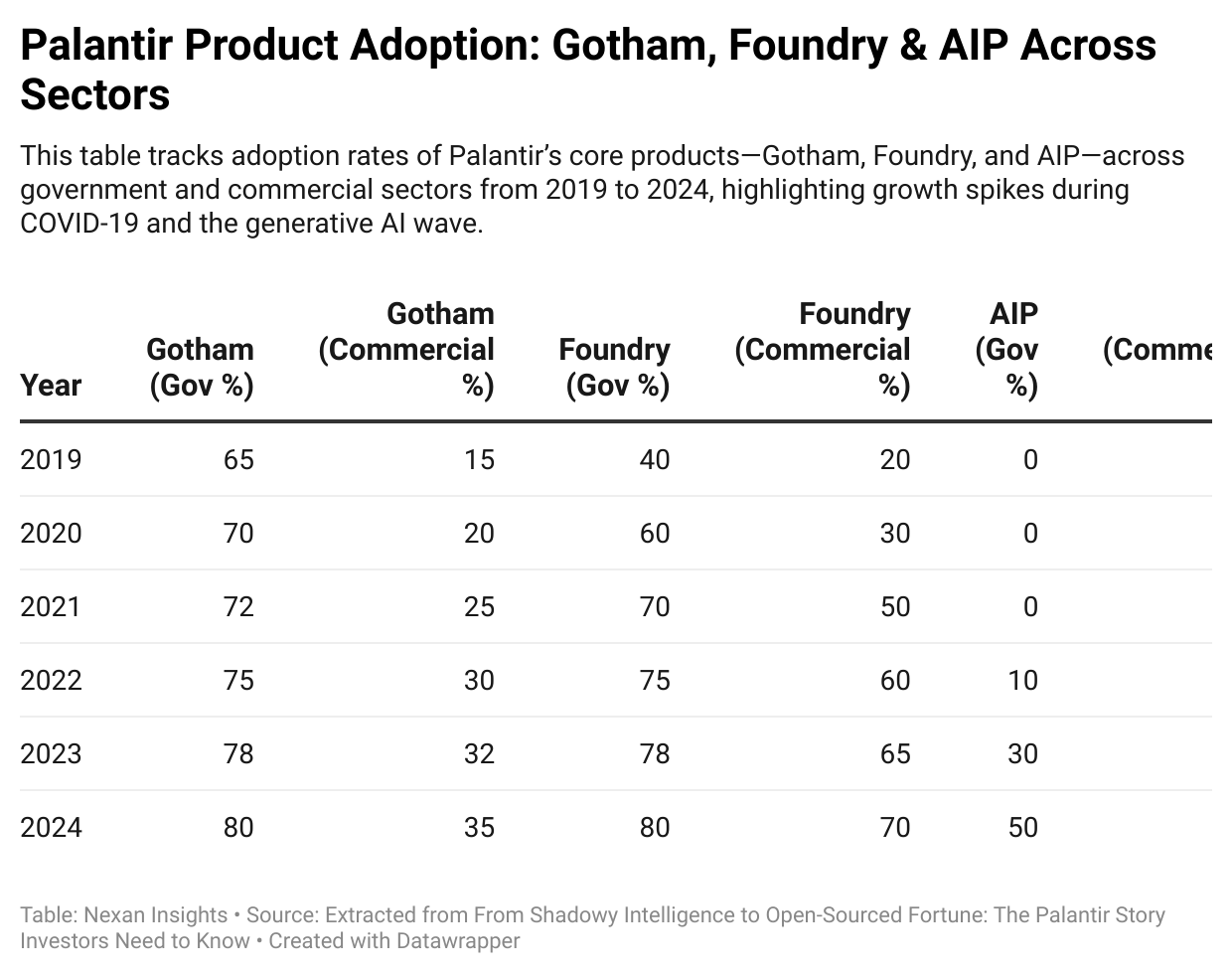

This table tracks adoption rates of Palantir’s core products—Gotham, Foundry, and AIP—across government and commercial sectors from 2019 to 2024, highlighting growth spikes during COVID-19 and the generative AI wave.

Palantir Technologies has evolved from a defense-focused data integrator into an enterprise AI platform competing across sectors. Its unique dual approach—leveraging consulting-heavy onboarding for sticky SaaS revenue and embedding within defense procurement ecosystems—has yielded consistent adoption across both public and commercial domains. With products like Gotham, Foundry, and the new AIP interface, Palantir positions itself as the intelligence layer atop fragmented data systems. While geopolitical tailwinds and innovation funds act as accelerants, barriers remain in global expansion and hardware-adjacent competition.

1. Market Structure: A Stack for Intelligence Across Domains

Palantir operates at the convergence of defense software, enterprise data infrastructure, and now generative AI. Its three product lines—Gotham (defense/intelligence), Foundry (enterprise ops), and AIP (LLM interface)—form a vertically integrated suite that consolidates ingestion, modeling, querying, and AI-layer deployment.

Gotham serves mission-critical military and intelligence clients by aggregating and contextualizing battlefield and threat data.

Foundry offers process visibility and optimization across fragmented ERP, CRM, and logistics systems.

AIP introduces a programmable interface layer atop structured enterprise data for generative AI applications.

This triad creates a unified data operating system, especially valuable to entities with legacy infrastructure and security concerns. Its architecture resembles Snowflake’s vertical integration but applied to high-stakes domains such as defense planning, supply chain continuity, and energy logistics.

Product Adoption Growth (2018–2023):

Gotham saw consistent U.S. federal contract growth under OTAs and IDIQ frameworks.

Foundry gained commercial traction during COVID-19 for supply chain visualization.

AIP usage accelerated post-2023 with the generative AI wave, driven by structured LLM deployment atop existing Foundry stacks.

Adoption growth of Palantir’s Gotham, Foundry, and AIP across sectors (2018–2023).

2. Growth Constraints: Bureaucracy as Both Moat and Brake

Palantir’s deep roots in U.S. government contracting remain both a strength and a constraint.

Key mechanisms for access and growth:

OTA (Other Transaction Authority): Enables rapid prototyping outside FAR constraints.

IDIQ (Indefinite Delivery/Indefinite Quantity): Provides modular expansion without rebidding.

SBIR/DIU/AFWERX: Enable early-stage innovation funding, often leading to Programs of Record.

While this access secures long-term footholds, it limits agility. Contracts span years, require extensive compliance, and expose Palantir to macro-level budgetary cycles. The path from prototype to DoD-wide adoption is long, with funding often disjointed across federal silos.

Visualizing the complex maze of U.S. government contract pathways—OTA, IDIQ, SBIR—that defense tech startups must navigate.

3. Competitive Landscape: Intelligence vs. Hardware Supremacy

Palantir faces asymmetric competition. Unlike pure SaaS players, its rivals often include hardware-first defense contractors like Anduril.

Anduril: Vertical integration from sensor to strike capability, with native software control.

Palantir: Specializes in software-defined situational awareness, reliant on external hardware.

Programs like TITAN (Tactical Intelligence Targeting Access Node) reflect this collision. TITAN demands real-time software insights deployed on battlefield-grade hardware—a convergence of Palantir’s software stack with military-grade compute and connectivity.

While Palantir holds the upper hand in complex data modeling, its lack of vertical control over hardware creates dependency risk. Integration partnerships and modular software deployment are key to preserving strategic leverage.

A visual breakdown of how Palantir’s revenue shifts from consulting-heavy to product-driven as client relationships mature.

4. Distribution Model: From Consulting Footprint to SaaS Leverage

Palantir’s model begins with high-touch deployments resembling management consulting, followed by conversion to recurring software revenue.

Revenue Evolution:

Initial Phase: Engineering-intensive onboarding, often subsidized or funded via innovation grants (e.g., SBIR, DIU).

Maturity Phase: License-based revenue model with long-term stickiness.

Expansion Phase: Cross-sell via AIP modules, monetizing additional LLM queries and domain-specific agents.

This resembles the traditional B2B ERP sales cycle, but with higher upfront costs due to the bespoke nature of deployments. While this has raised criticism about scalability, customer retention metrics (e.g., net expansion rates) remain strong due to deep integration.

The battle between software intelligence (Palantir) and hardware innovation (drone warfare) in modern defense strategy.

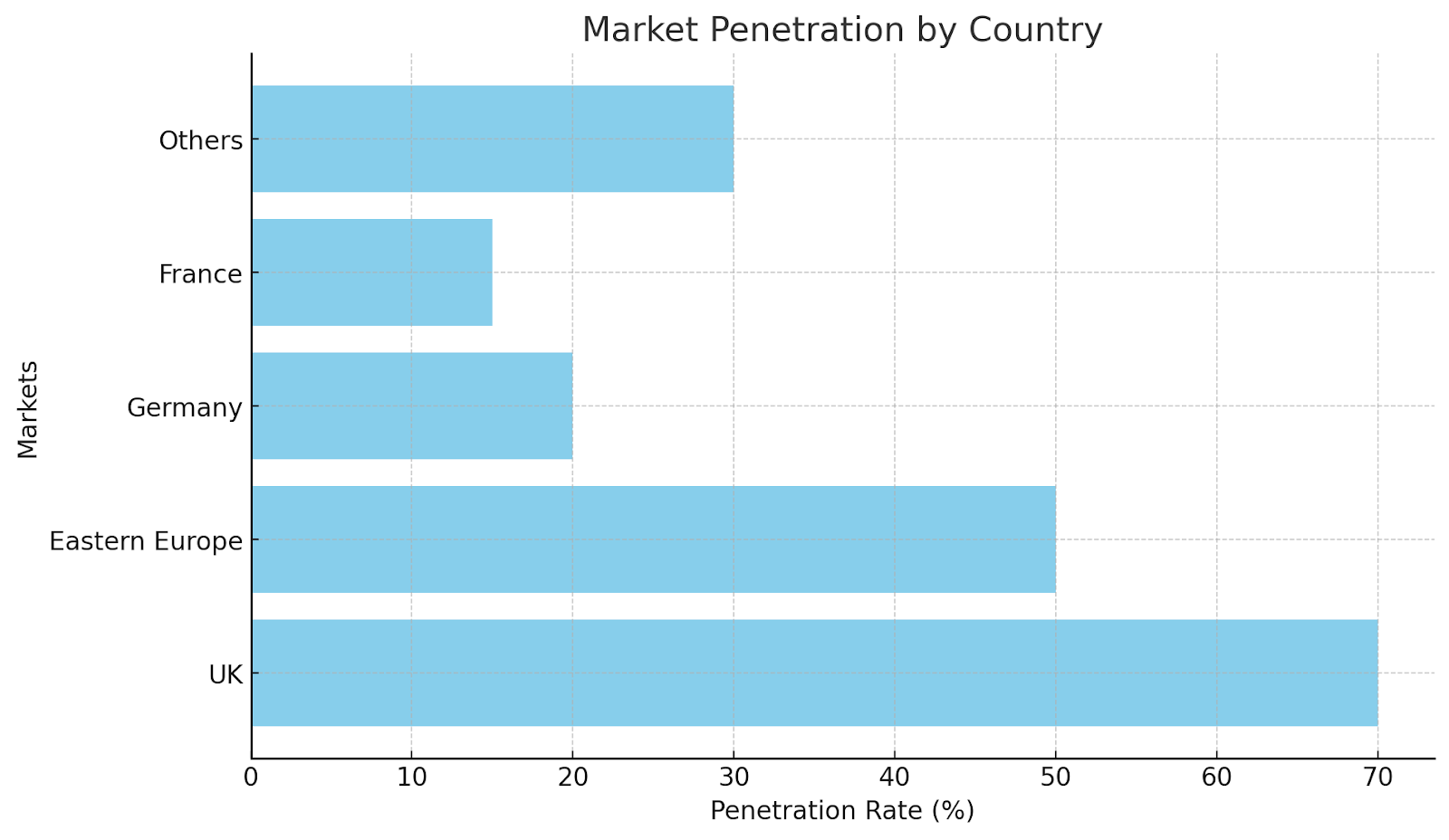

5. Supply Chain & International Hurdles: AIP as Trojan Horse

Palantir’s global push reveals structural frictions.

Adoption-friendly nations: UK, Ukraine, Poland—nations with acute defense or healthcare crises.

Adoption-resistant nations: France, Germany—entrenched public sector software ecosystems and wariness of U.S. surveillance tech.

In these markets, AIP plays a subtler role. Its positioning as a modular, interface-first product offers a lighter-weight entry point. AIP avoids some of the “data sovereignty” red flags associated with full-stack solutions like Foundry or Gotham.

However, challenges remain:

Data localization laws hinder AIP deployment if underlying data is stored or processed in U.S. jurisdictions.

Procurement inertia in the EU favors incumbent software vendors and public-private R&D consortiums.

Palantir's strongest market presence lies in the UK and Eastern Europe, with slower traction in France and Germany.

6. Innovation Programs as Catalysts: Not All Dollars Are Equal

Palantir’s growth is intertwined with innovation funding structures:

Program | Focus | Follow-on Conversion Potential |

|---|---|---|

SBIR | Early-stage innovation | Moderate |

DIU | Rapid prototyping for defense | High |

AFWERX | Air Force-centric tech | Medium |

DIU stands out for its higher transition rate into Programs of Record—full-scale adoption across DoD units. Palantir’s success in winning DIU awards signals institutional trust and increases downstream contract conversion potential.

Investors should monitor:

Climbing the innovation funding ladder—SBIR and DIU are key stepping stones to full-scale adoption for defense tech like Palantir.

7. Strategic Convergence: Platformization of Intelligence

Palantir’s long-term thesis lies in convergence—not just of products, but of data, use cases, and user interfaces.

Gotham + Foundry form the substrate for multi-domain operational planning.

AIP adds intuitive access to this infrastructure, enabling broader personnel to leverage LLMs without deep engineering support.

This creates a self-reinforcing loop:

High-value institutions install Foundry or Gotham.

Internal users expand usage via AIP.

Upsells increase as predictive use cases (e.g., logistics forecasting, threat simulation) are unlocked.

This mirrors Snowflake’s pattern of usage growth via workloads rather than user seats—except Palantir’s workloads are often defense or national infrastructure critical.The convergence of Palantir’s product suite—Gotham, Foundry, and AIP—into a unified, enterprise-grade intelligence platform.

Takeaways: Operator & Investor Implications

Product-Led Growth With a Consulting Front-End

Expect high CAC but strong lifetime value, driven by deep entrenchment within client operations.Government as Growth Flywheel

Winning DIU, OTA, or SBIR contracts is more than revenue—it’s pipeline for broader agency adoption.AI Democratization as Retention Strategy

AIP ensures non-technical users can interface with structured data. This democratization enhances renewal and upsell probability.Hardware-Software Integration Is the Next Battleground

Partnerships or acquisitions in edge compute or ruggedized AI hardware may become strategic necessities.Global Market Still Nascent

Success in Europe hinges on product modularity, localization compliance, and reframing of U.S.-centric brand.

Palantir is not a pure-play SaaS, nor a classic defense contractor. It is building the intelligence layer between fractured public infrastructure, enterprise systems, and the AI era’s operational needs. For investors and operators alike, understanding this hybrid DNA is critical to assessing its asymmetric advantage.