- Nexan Insights

- Posts

- How Synopsys and Cadence Power the Semiconductor Revolution

How Synopsys and Cadence Power the Semiconductor Revolution

Exploring the competitive landscape, SaaS transition, and AI-driven growth fueling the future of chip design.

Ajit Banerjee

April 09, 2025

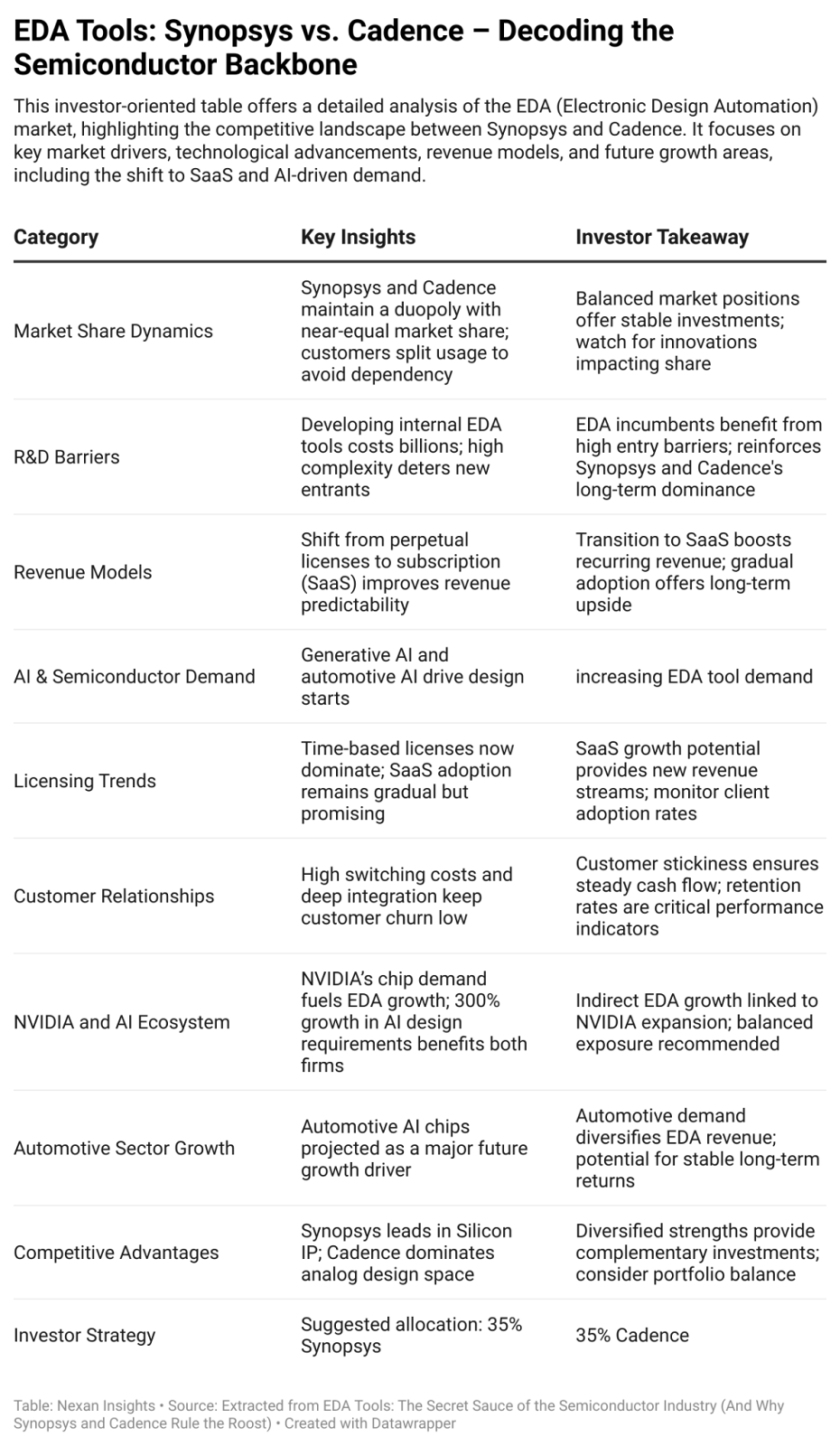

This investor-oriented table offers a detailed analysis of the EDA (Electronic Design Automation) market, highlighting the competitive landscape between Synopsys and Cadence. It focuses on key market drivers, technological advancements, revenue models, and future growth areas, including the shift to SaaS and AI-driven demand.

Synopsys and Cadence dominate the Electronic Design Automation (EDA) industry, providing essential design tools that underpin the global semiconductor supply chain. This report examines the EDA market structure, technological evolution, SaaS transformation, and AI-driven growth vectors—framing them through the lens of investor implications, competitive dynamics, and future scaling opportunities.

1. EDA Tools: The Blueprint of the Semiconductor Age

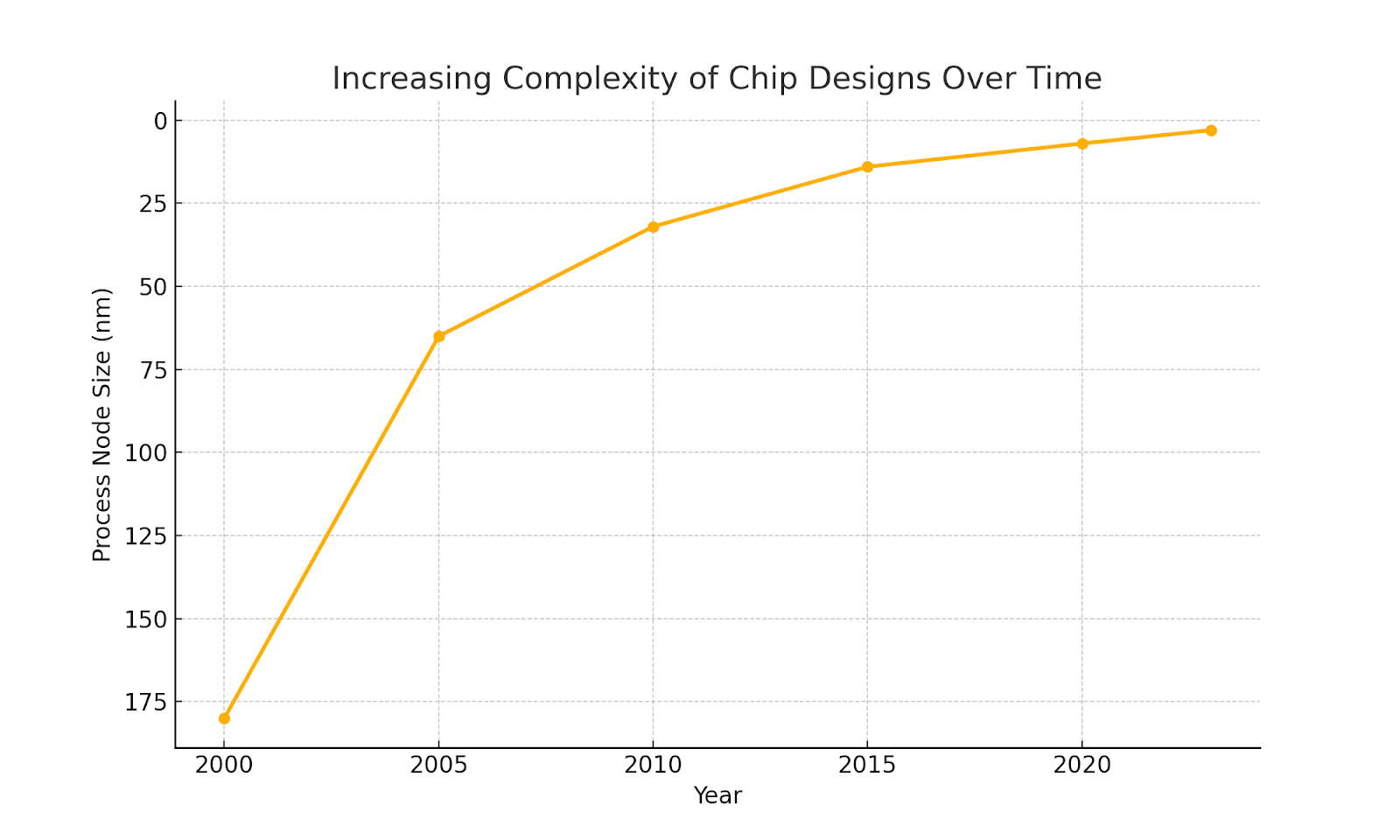

Modern chip design resembles urban planning at atomic scale—millions of transistors, gates, interconnects, and power domains integrated under strict performance and thermal constraints. Electronic Design Automation (EDA) software serves as the architecture suite, simulating, verifying, and optimizing these integrated circuits.

EDA tools are used by every major semiconductor manufacturer—including NVIDIA, Apple, Intel, AMD, Qualcomm, and Broadcom.

Each new chip design iteration (a “design start”) increases licensing revenue for EDA vendors.

Estimated chip complexity has doubled roughly every 18–24 months, increasing EDA workloads and license value per design.

Caption: EDA tools compress the complexity of New York City into nanometers of silicon, driving power, performance, and integration at scale.

Increasing chip complexity drives higher demand for EDA tools.

EDA tools: Designing microchips as complex as New York City—power, efficiency, and connectivity all compressed into silicon.

2. Market Entry: Why EDA is an Impenetrable Fortress

Despite their strategic importance, EDA vendors remain few due to extreme market entry barriers:

Technical depth: Requires decades of expertise in physics-based modeling, logic synthesis, and foundry process alignment.

Customer embeddedness: Tools are deeply integrated into chipmakers’ workflows—replacing them risks billions in product delays.

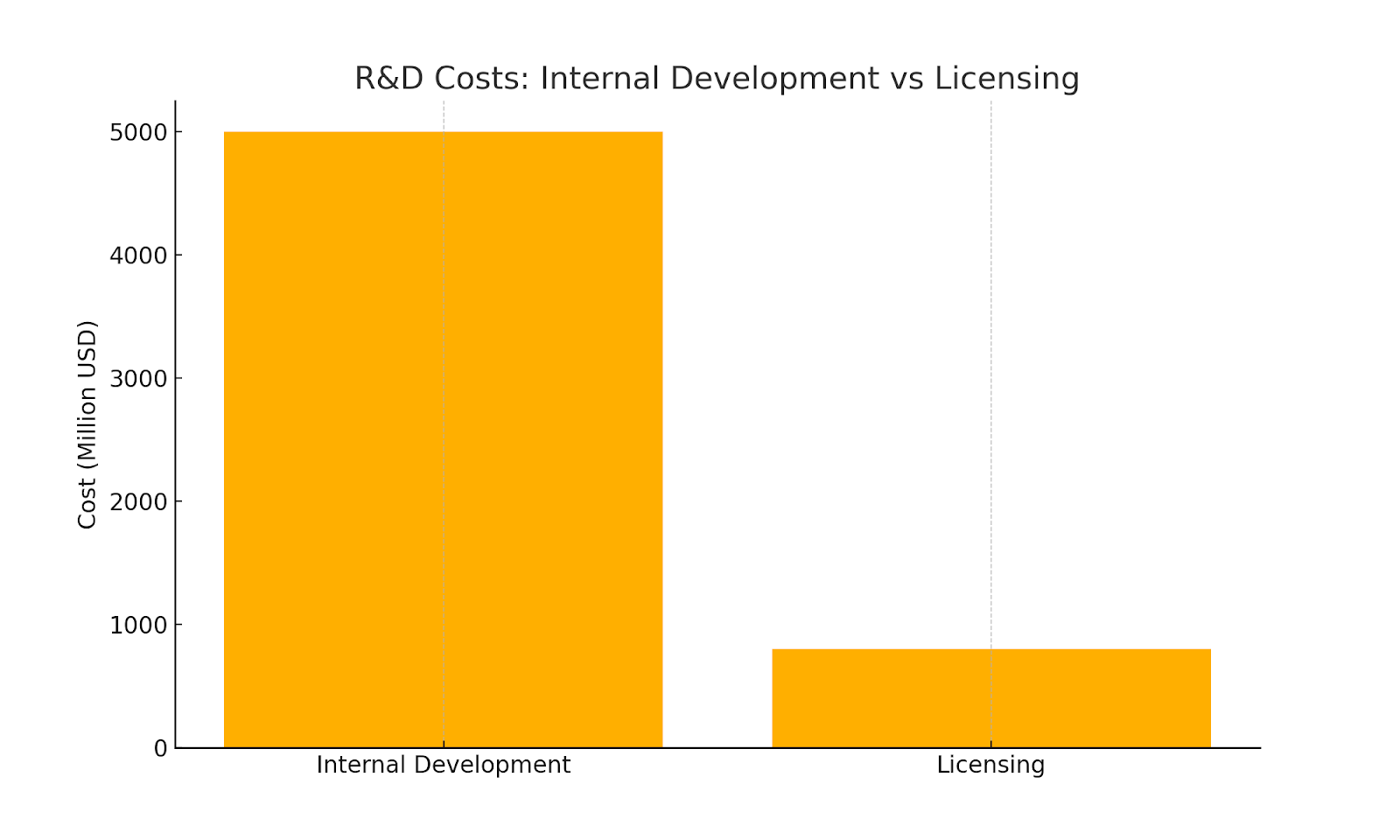

R&D burden: An in-house EDA stack can cost billions to develop without scale economies.

As former Synopsys executives have noted, even a firm like NVIDIA would incur steep costs with minimal ROI attempting internal tool replication.

Caption: EDA incumbents lock out competition through engineering depth, legacy integration, and risk mitigation advantages.

R&D costs soar with internal development—licensing proves a far more cost-effective choice.

Synopsys and Cadence dominate the EDA industry, leveraging high R&D costs and strong customer relationships to maintain significant entry barriers.

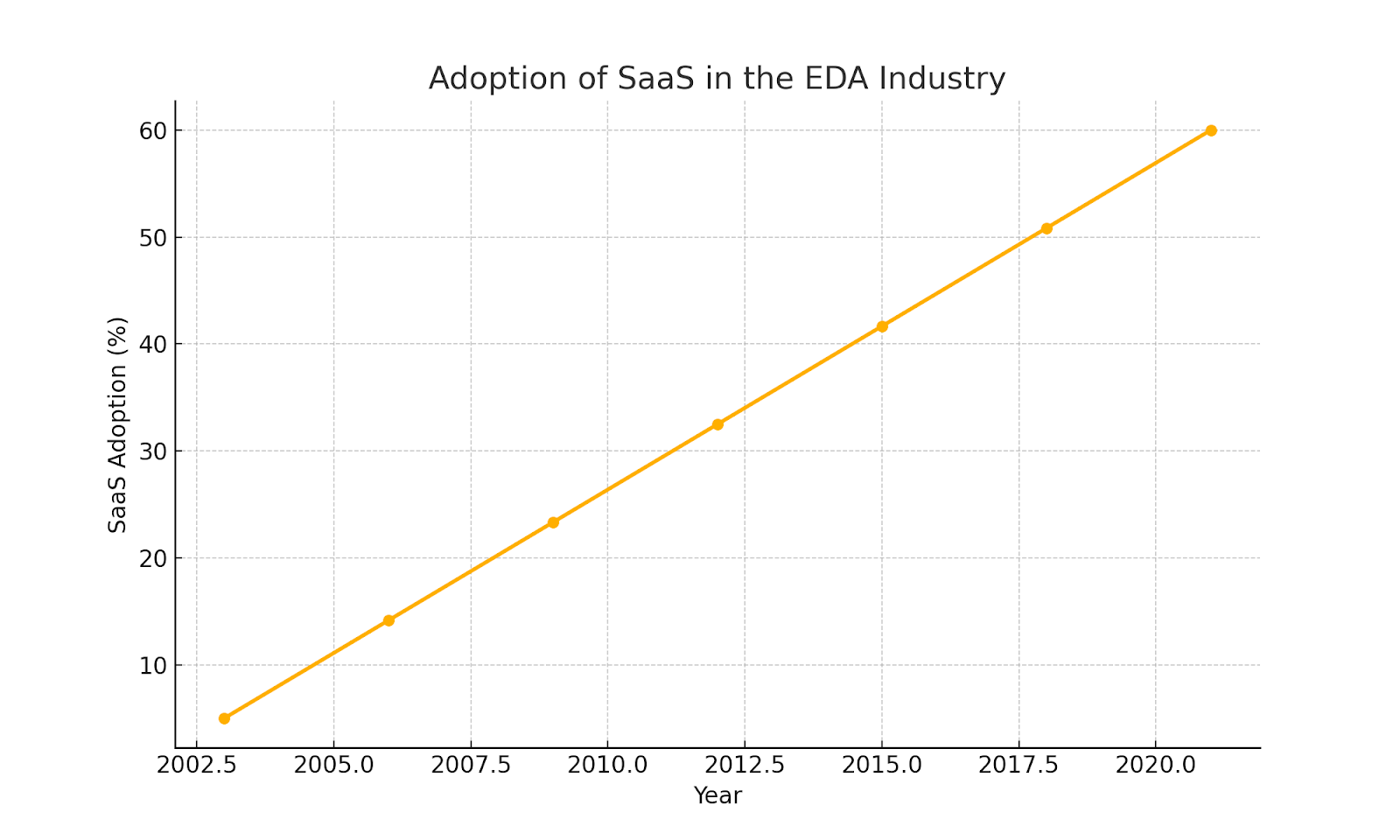

3. Business Model Evolution: From Perpetual to SaaS Licensing

EDA licensing models have transitioned over two decades:

Pre-2003: Perpetual licenses with optional maintenance

2003–2020: Term-based licensing every 2–3 years, improving revenue visibility

2020–present: Shift toward cloud-native SaaS (e.g., Synopsys Cloud, Cadence OnCloud)

The move to SaaS introduces pricing flexibility and usage-based scalability, but adoption is slowed by semiconductor firms’ preference for cost predictability and IP control.

Caption: EDA’s SaaS evolution mirrors broader enterprise software trends, but adoption lags due to sensitivity around design IP and compute costs.

SaaS adoption in the EDA industry has steadily increased, reaching 60% by 2021, highlighting the shift towards flexible, subscription-based models.

EDA licensing shifts from one-time payments to flexible SaaS models.

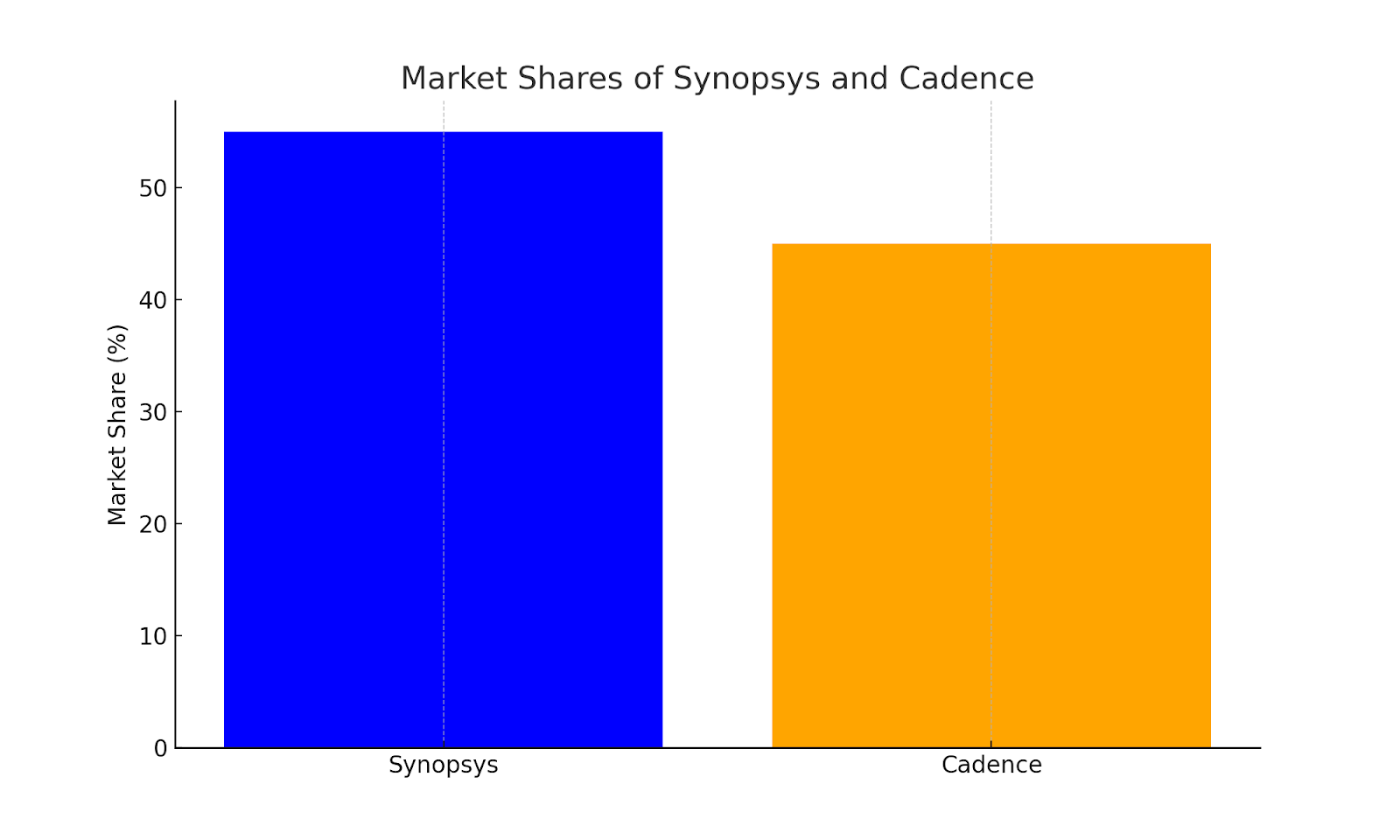

4. Competitive Dynamics: Synopsys vs. Cadence in a Duopolistic Truce

Synopsys and Cadence represent a rare case of stable duopolistic competition:

Company | Primary Strength | Secondary Focus |

|---|---|---|

Synopsys | Digital Design Tools, Silicon IP | Cloud/SaaS Integration, Verification |

Cadence | Analog/RF Design, Simulation | System Design, Thermal Modeling |

Most large customers (e.g., Apple, Qualcomm) maintain licenses with both vendors to reduce dependency risk.

Competitive tension drives innovation but prevents margin erosion—a rare balance.

Caption: Synopsys and Cadence compete without disruption, preserving pricing power and product velocity through mutual deterrence.

Synopsys leads the EDA market with a slight edge over Cadence.

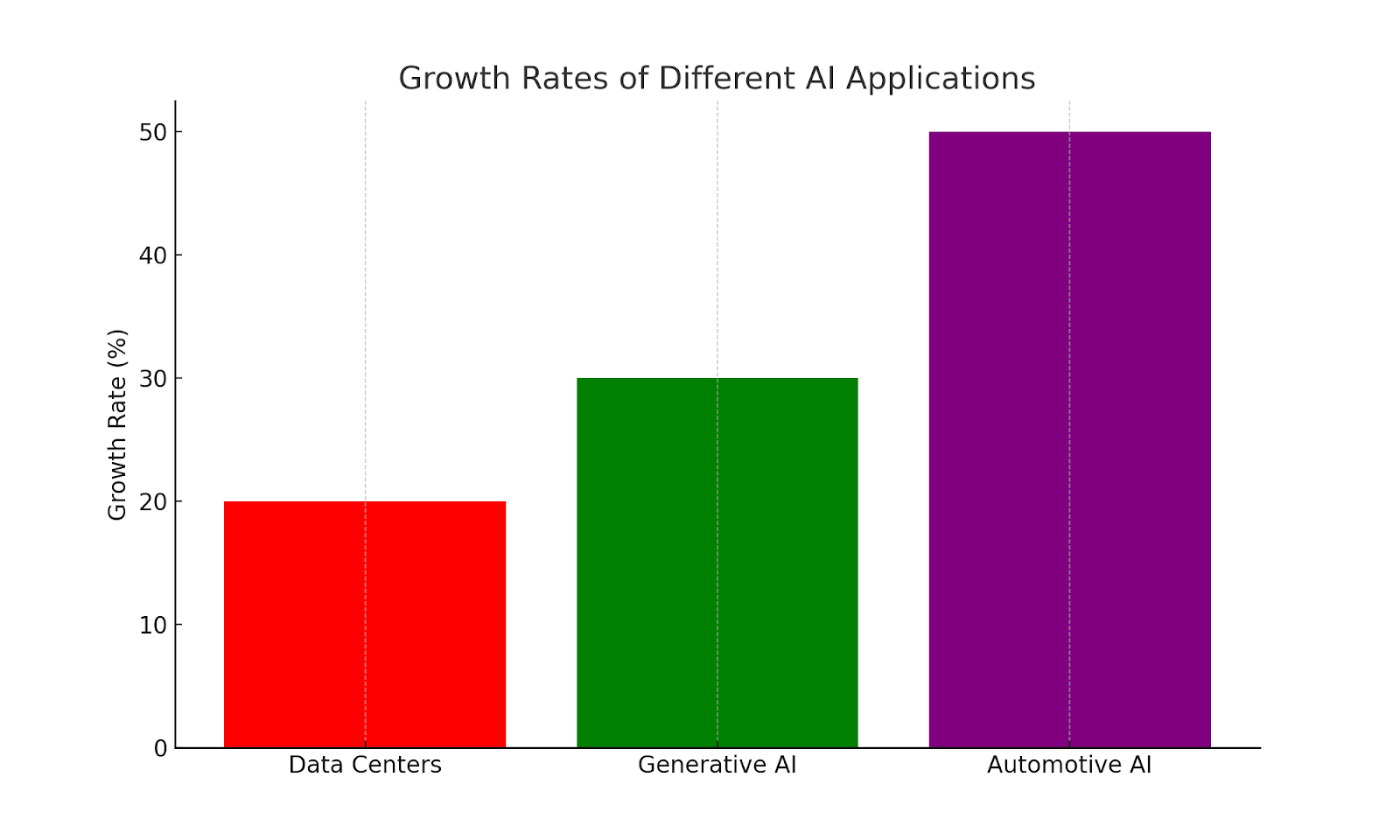

5. AI and Design Starts: The Demand Flywheel for EDA

Generative AI and edge AI are expanding the semiconductor design frontier:

NVIDIA’s growth (triple-digit YoY in some segments) has catalyzed demand for more GPUs and AI accelerators.

Automotive AI (ADAS, autonomous driving SoCs) is the fastest-growing segment, with design starts increasing sharply.

Each new AI hardware segment feeds directly into EDA revenue through tool licensing and simulation workloads.

Caption: AI’s growth creates a multiplier effect for EDA tools: more chips, more designs, more simulations.

Automotive AI leads with the highest growth rate among AI applications.

Automotive AI accelerates ahead as the fastest-growing segment among AI applications.

6. Investor Strategy: Balanced Allocation with Optionality

Synopsys and Cadence offer:

High gross margins (~85%)

Strong cash flow generation

Moderate but durable growth tied to semiconductors' long-term trajectory

Investment frameworks suggest:

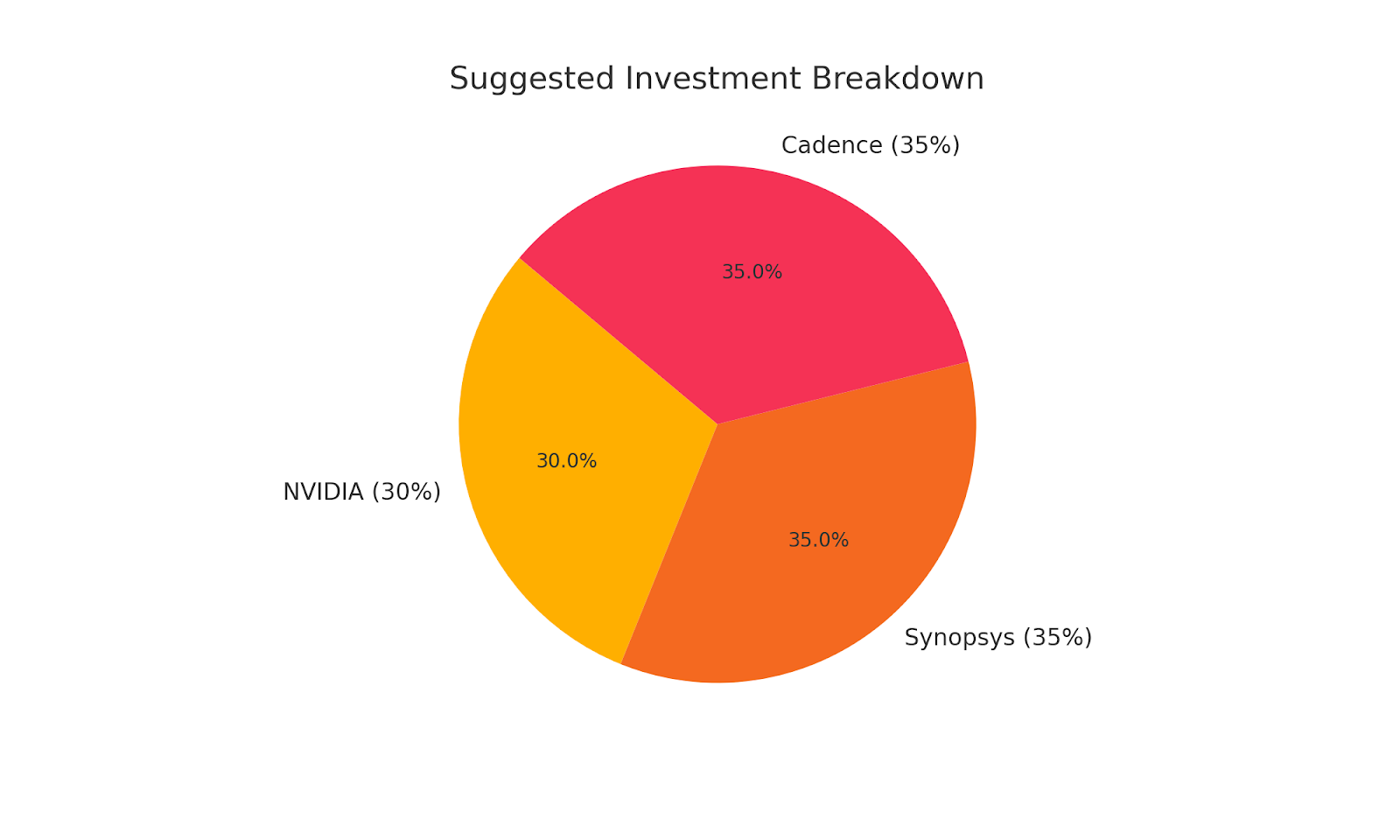

70% capital allocation to Synopsys + Cadence for defensive exposure

30% optionality in NVIDIA or emerging AI hardware for growth acceleration

Caption: A dual investment in Synopsys and Cadence offers defensible cash flow, while NVIDIA adds upside volatility.

Balanced investment approach: 70% in Synopsys and Cadence for stability, 30% in NVIDIA for high growth potential.

Diversified strategy: 70% in Synopsys and Cadence for long-term growth, 30% in NVIDIA for short-term high-risk investment.

7. Long-Term Thesis: Infrastructure Beneath the Infrastructure

Unlike consumer-facing semiconductor giants, Synopsys and Cadence operate in the background—enabling every chip design before it’s manufactured. They are infrastructure providers in a market where failures are unaffordable and reliability is paramount.

As long as compute demand increases and transistor scaling continues, EDA demand remains structurally secure.

Caption: EDA firms are the invisible hands behind every silicon advancement—quiet giants shaping the digital age.

Takeaways: Operator and Investor Insights

Structural Advantage: EDA remains a high-barrier niche with durable demand and pricing power.

SaaS Upside: While adoption is slow, SaaS transition may unlock ARR growth and customer expansion in underserved markets.

AI-Driven TAM Expansion: Each wave of AI, automotive, and edge compute drives incremental tool consumption.

Balanced Strategy: Synopsys (IP + digital) and Cadence (analog + simulation) offer complementary exposure with minimal overlap.

For institutional capital seeking stable exposure to the semiconductor cycle with less volatility than chipmakers themselves, EDA vendors provide a resilient and compounding corner of the value chain.