- Nexan Insights

- Posts

- The Complicated and Surprisingly Fascinating World of Handbags in Indian E-Commerce

The Complicated and Surprisingly Fascinating World of Handbags in Indian E-Commerce

A Tim Urban Dive

Ajit Banerjee

May 17, 2025

This table highlights the segmentation, competitive positioning, and challenges of the Indian handbag market, focusing on the organized versus unorganized segments, growth rates, top brands, and distribution strategies.

India’s ₹4,000 crore organized handbag market—long a story of rapid digital growth—has reached a phase of structural complexity and decelerating expansion. As growth plateaus and digital penetration slows, success increasingly hinges on supply chain adaptability, direct-to-consumer models, and strategic differentiation. Brands like Zouk and Lavie exemplify operational agility, while legacy players such as Caprese face stagnation due to structural inertia. This report dissects the Indian handbag sector through the lenses of market segmentation, competitive dynamics, distribution shifts, and operational resilience.

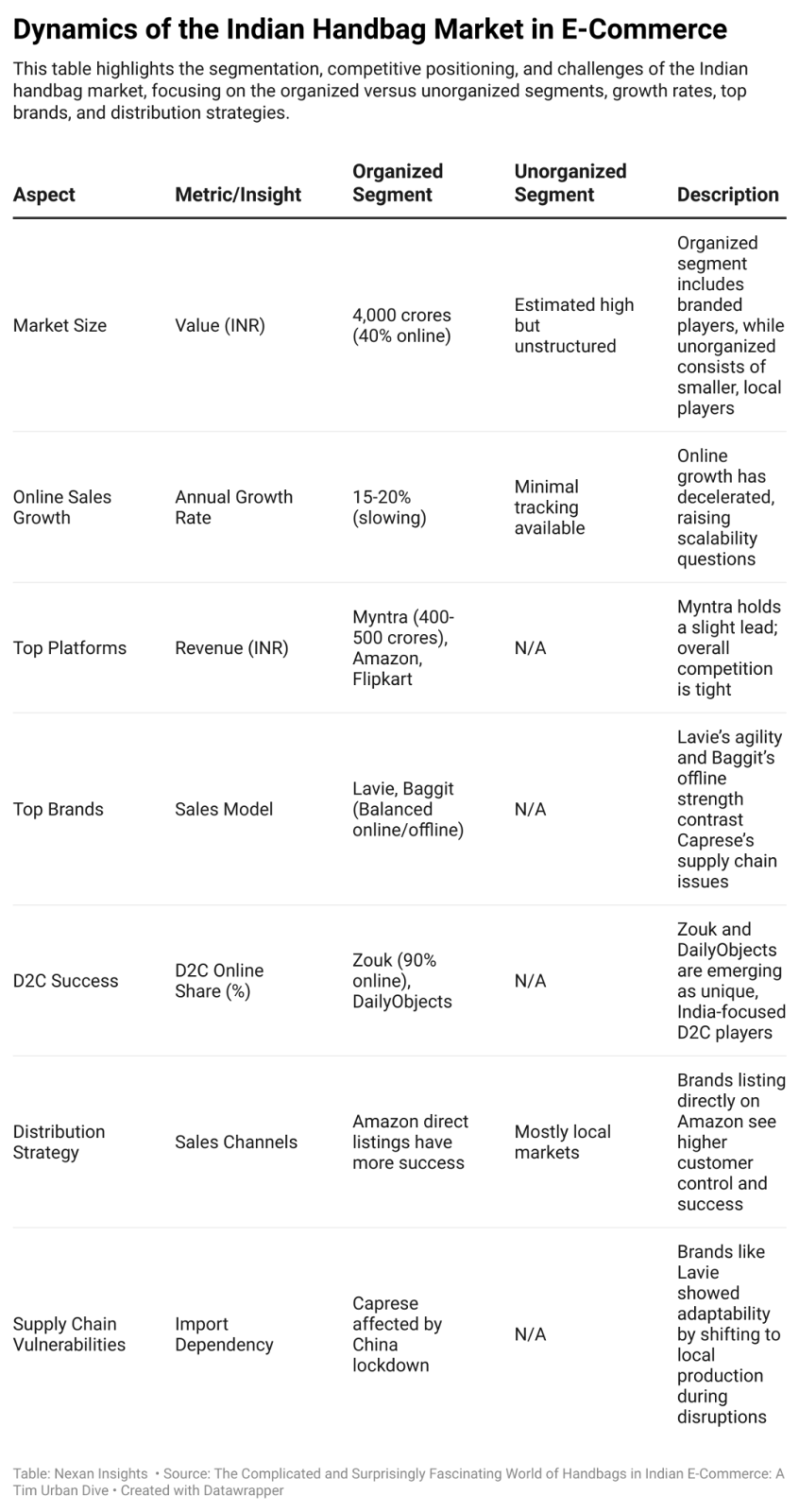

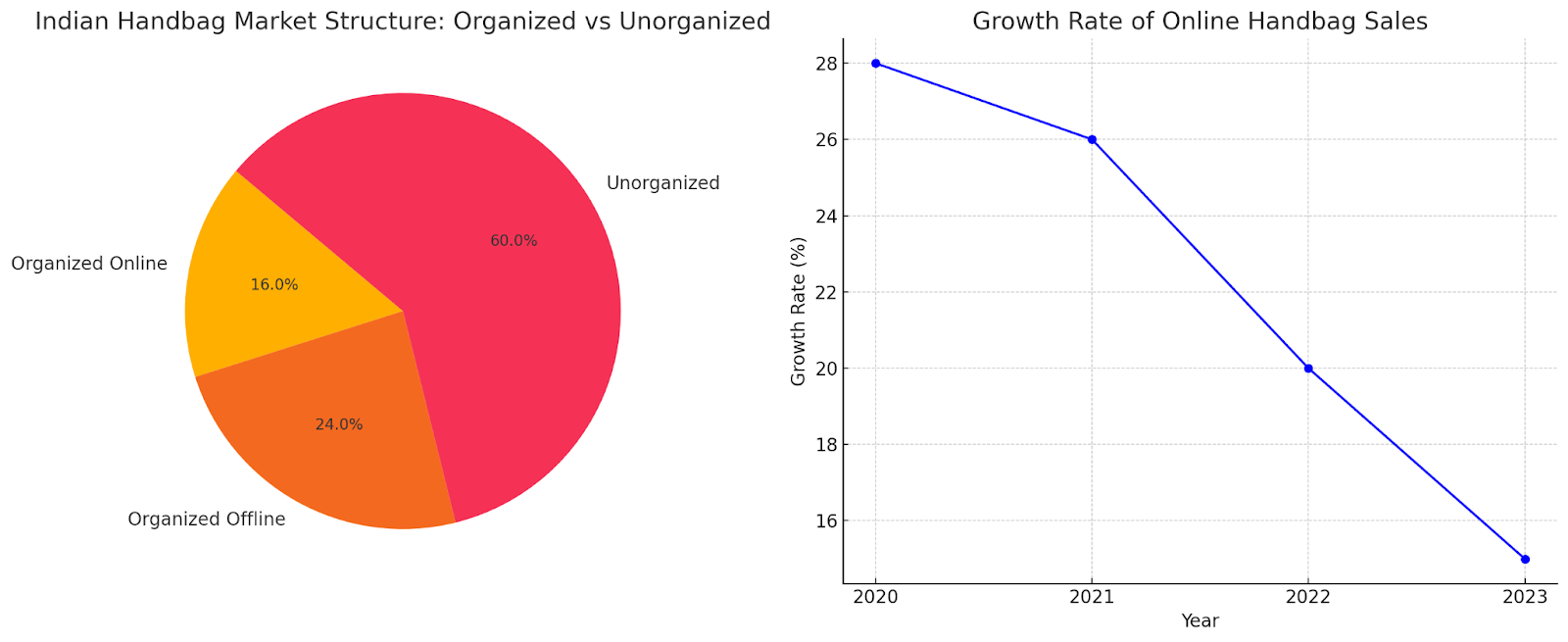

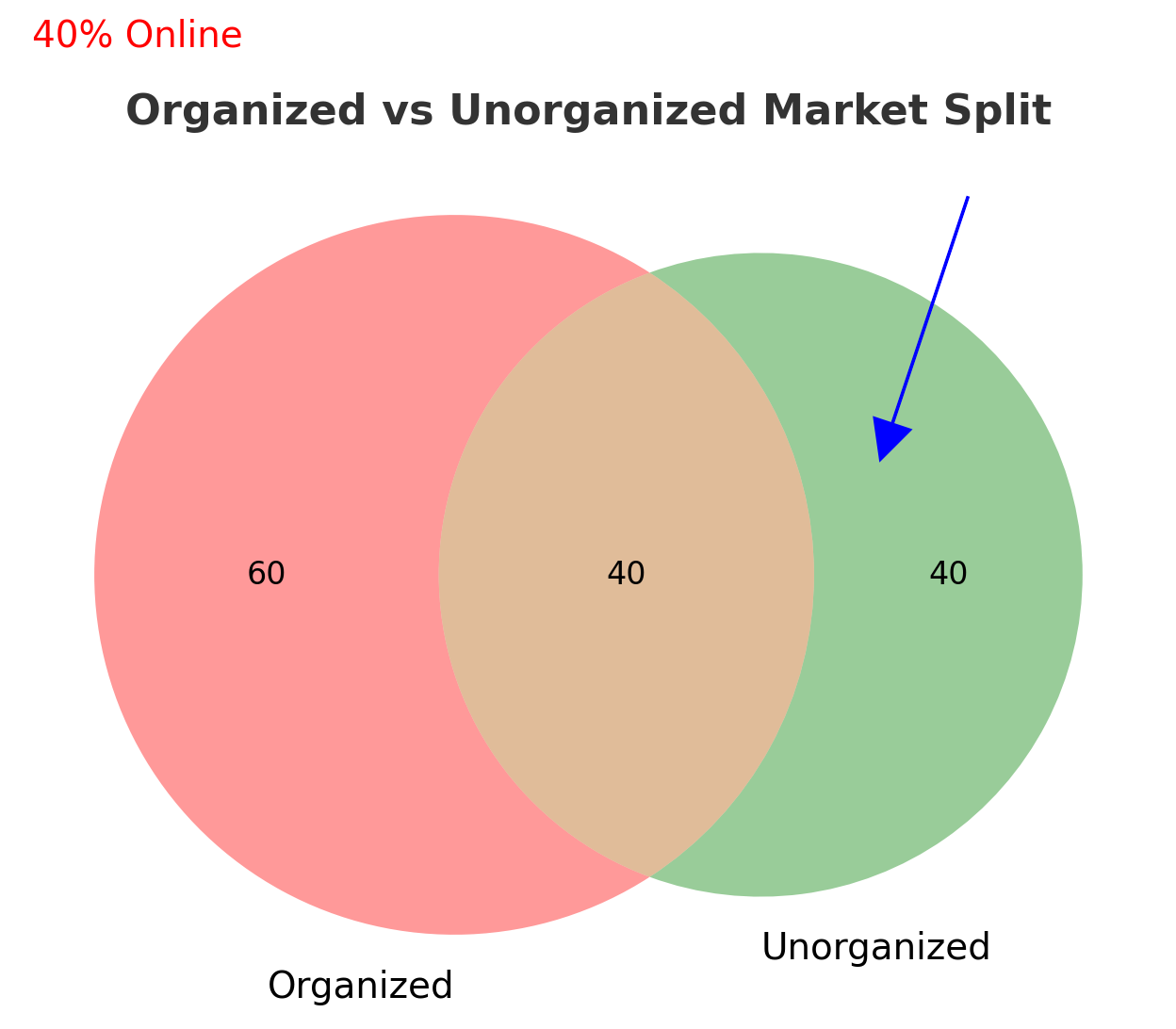

1. Market Structure: A Split Between Order and Chaos

India’s handbag industry is bifurcated: a fragmented 60% unorganized segment versus a ₹4,000 crore organized market. Organized retail continues to gradually expand its footprint, with roughly 40% of its value now flowing through online channels. However, once-robust e-commerce growth of 25–30% YoY has moderated to 15–20%, marking the early signs of digital saturation.

Segment | Value (INR Crore) | Share | Online Penetration |

|---|---|---|---|

Organized | ~4,000 | 40% | 40% |

Unorganized | ~6,000 | 60% | Negligible |

This deceleration points to an emerging ceiling in India’s digital retail addressable market for mid-tier consumer fashion items. As informal players digitize more slowly, formal players must extract more value from an increasingly saturated e-commerce base.

India’s Handbag Market Snapshot – A 60% unorganized market contrasts with slowing online growth, signaling both the dominance of informal players and the challenges ahead for digital retail expansion.

Organized vs. Unorganized Market Split – A Venn view of India's handbag market reveals a 40% overlap now online, as brands navigate the push from traditional structures to digital growth.

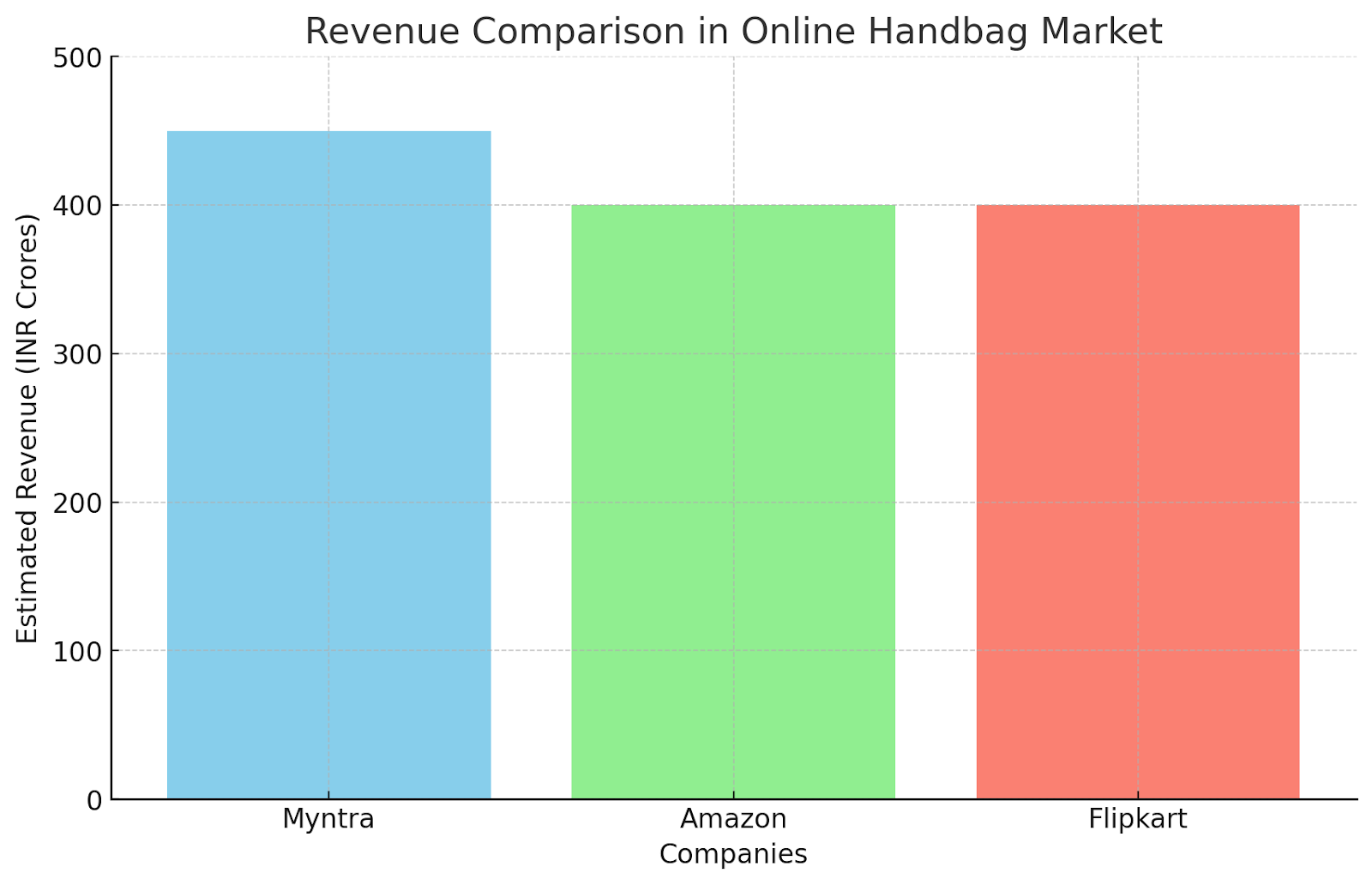

2. Growth Constraints: Platforms Struggle to Differentiate

Myntra, Amazon, and Flipkart dominate India’s online handbag ecosystem, sharing an estimated ₹1,400 crore opportunity. Myntra holds a slim lead (~₹450 crore), but growth across platforms is flattening. The absence of clear product or service differentiation renders this space a commodity market—where price sensitivity, logistics efficiency, and UI/UX parity mean there are few moats left.

Platform | Estimated GMV (Handbags) | Observed Trend |

|---|---|---|

Myntra | ₹400–₹500 crore | Marginal lead, stable |

Amazon | ₹350–₹450 crore | Steady |

Flipkart | ₹350–₹450 crore | Steady |

This environment drives intensified CAC pressure, promotional spend, and inventory turnover stress. Strategic expansion into premium SKUs or white-labeled offerings could provide future upside if executed with precision.

Platform Revenue Race – Myntra leads the online handbag market with estimated revenues around ₹450 crores, edging out Amazon and Flipkart in a tightly contested e-commerce arena.

Hikers on the Handbag Hill – Myntra, Amazon, and Flipkart climb a steep e-commerce slope, now flattening as growth in the online handbag market begins to level off.

3. Competitive Landscape: Agility Over Legacy

Brand differentiation plays a critical role in the sector’s long-term profitability. Direct-to-consumer (D2C) players like Zouk and DailyObjects command attention with cultural design cues and digitally native strategies. Zouk's 90% online D2C model, rooted in India-centric design language, offers an appealing mix of high gross margins and consumer resonance.

Brand | Channel Mix | Strategic Positioning | Recent Trends |

|---|---|---|---|

Zouk | ~90% online (D2C) | “Indian identity” design USP | Expanding into offline retail |

DailyObjects | >85% online (D2C) | Premium functional design | Gaining share in metro cities |

Lavie | 40% online | Fast adaptation to disruptions | Resilient post-COVID recovery |

Caprese | 20% online | Legacy offline brand | Declining due to supply chain |

Baggit | 20–30% online | Hybrid distribution model | Stagnant brand perception |

Caprese’s overreliance on Chinese imports left it exposed during COVID-era lockdowns, while Lavie benefited from rapid sourcing diversification and domestic production pivots. The contrast highlights how upstream flexibility now constitutes a core differentiator in consumer fashion logistics.

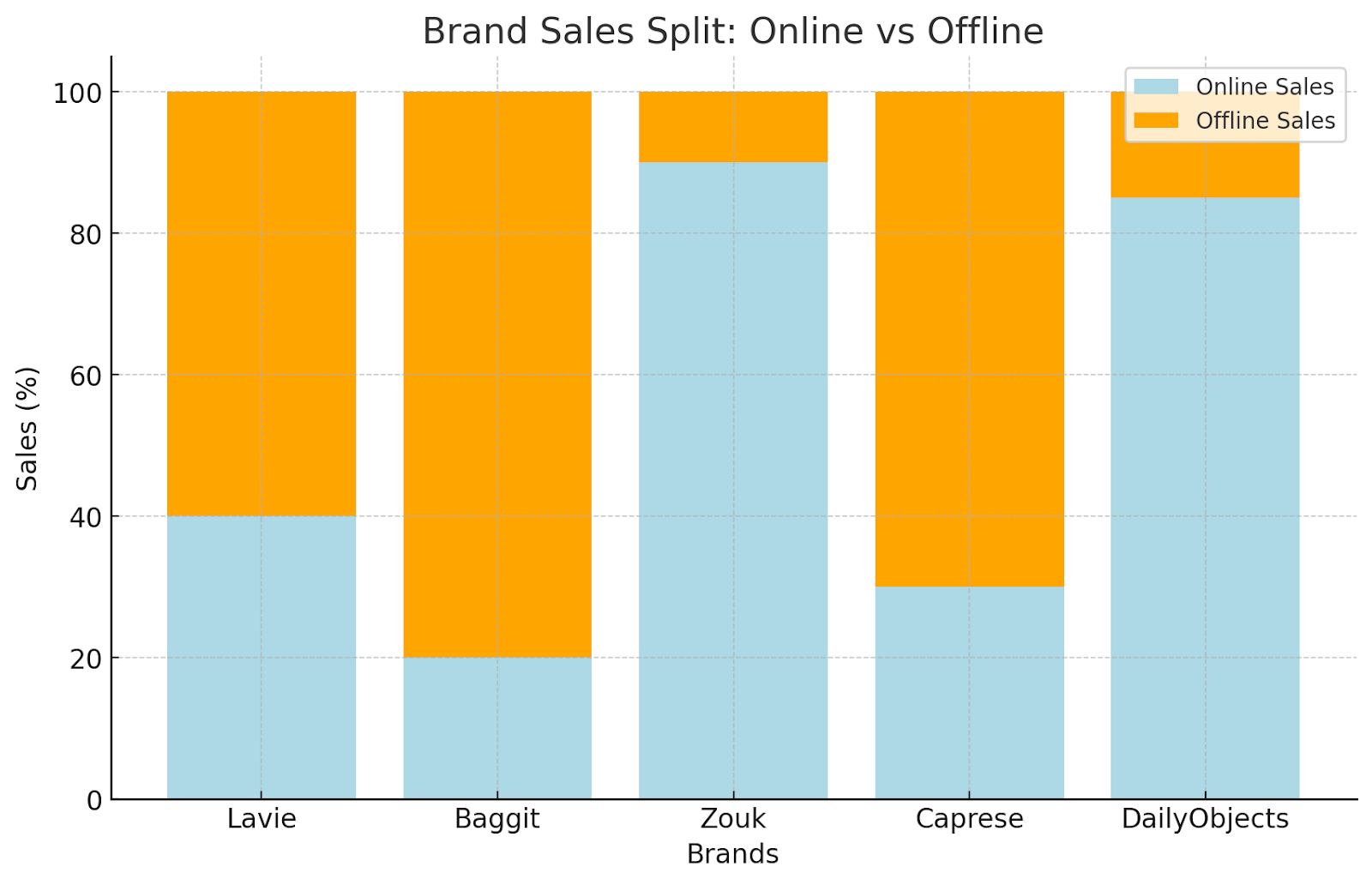

Online vs. Offline Brand Split – Zouk and DailyObjects lead the D2C wave with over 85% online sales, while Baggit and Caprese remain rooted in offline channels, highlighting contrasting distribution strategies.

Handbag Brands on the Playground – Zouk and DailyObjects wear the D2C crowns, Lavie works on supply chain fixes, while Caprese lags behind, weighed down by disruption and missed adaptation.

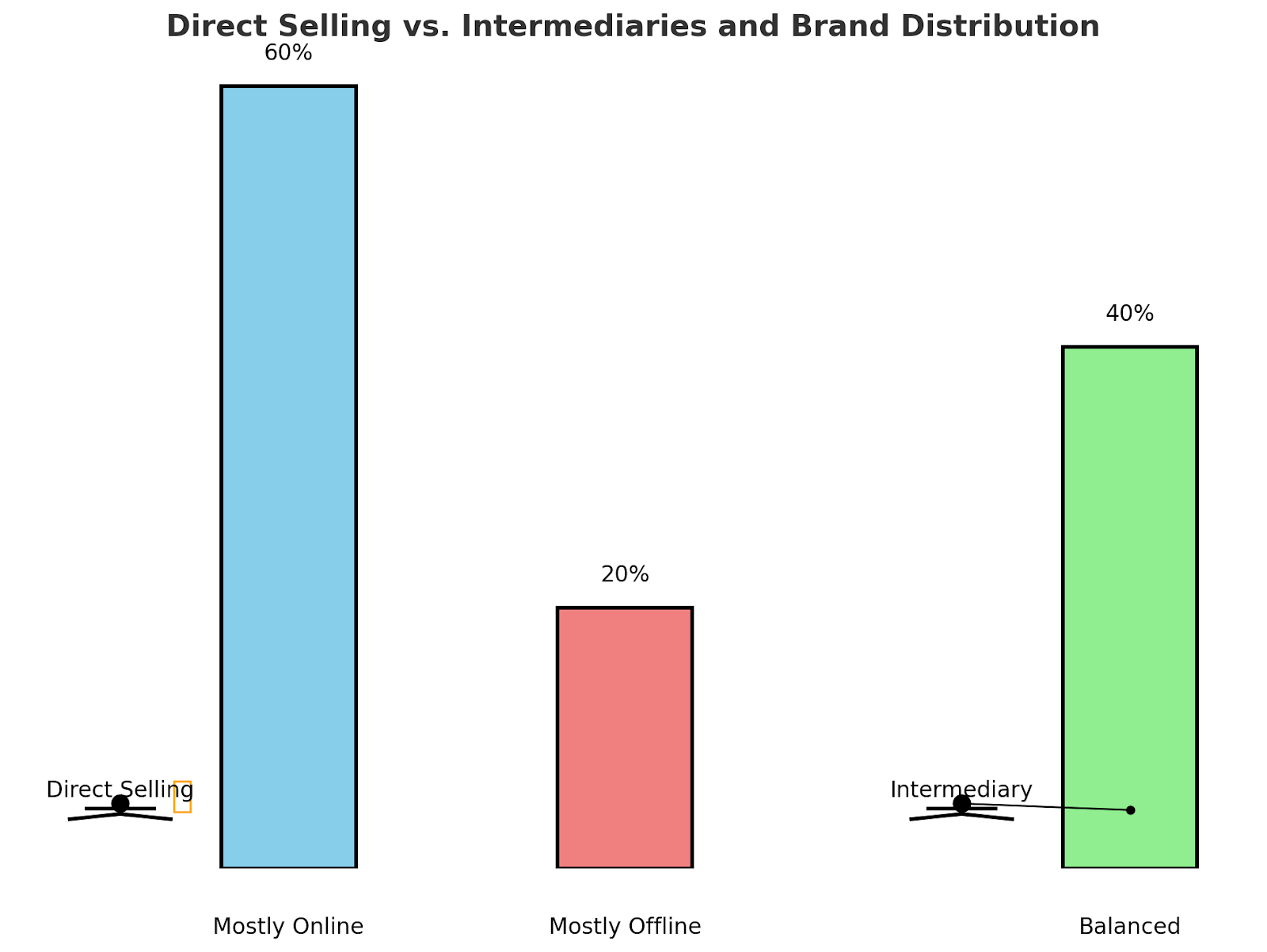

4. Distribution Models: D2C Dominance and Hybrid Tensions

Direct-to-consumer strategies offer margin optimization and consumer data control. Zouk and DailyObjects maximize control over pricing, branding, and fulfillment. Brands leveraging intermediaries or traditional offline channels, like Baggit and Caprese, are increasingly disadvantaged due to limited customer insight and slower iteration cycles.

Distribution Type | Notable Brands | Pros | Cons |

|---|---|---|---|

D2C Online | Zouk, DailyObjects | Higher margins, customer data | High CAC, limited offline scale |

Offline-Heavy | Baggit, Caprese | Retail presence, legacy trust | Inventory cost, low agility |

Hybrid | Lavie | Balanced reach, risk mitigation | Requires strong logistics backend |

Platforms like Amazon reward brands that list directly—enabling better control of product listings, reviews, pricing, and fulfillment. This offers a meaningful edge versus aggregator-led sales models, which obscure buyer-seller feedback loops.

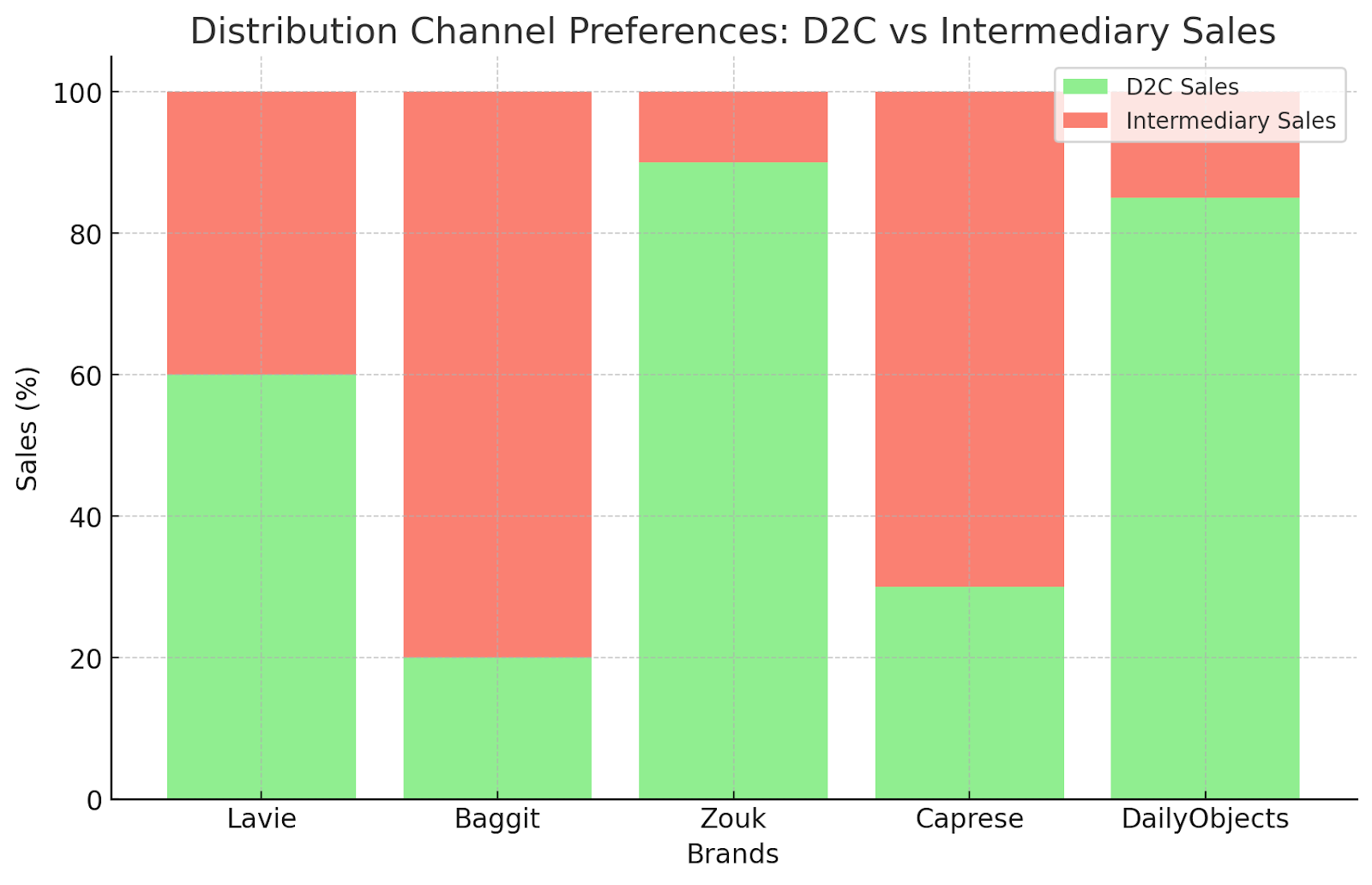

D2C vs. Intermediary Sales Split – Zouk and DailyObjects dominate with strong D2C strategies, while brands like Baggit and Caprese lean heavily on intermediaries, limiting control over customer experience.

Brand Distribution Breakdown – 60% of handbag brands lean toward direct online selling, while only 20% stay mostly offline, and 40% strike a balance—highlighting a clear shift toward D2C dominance.

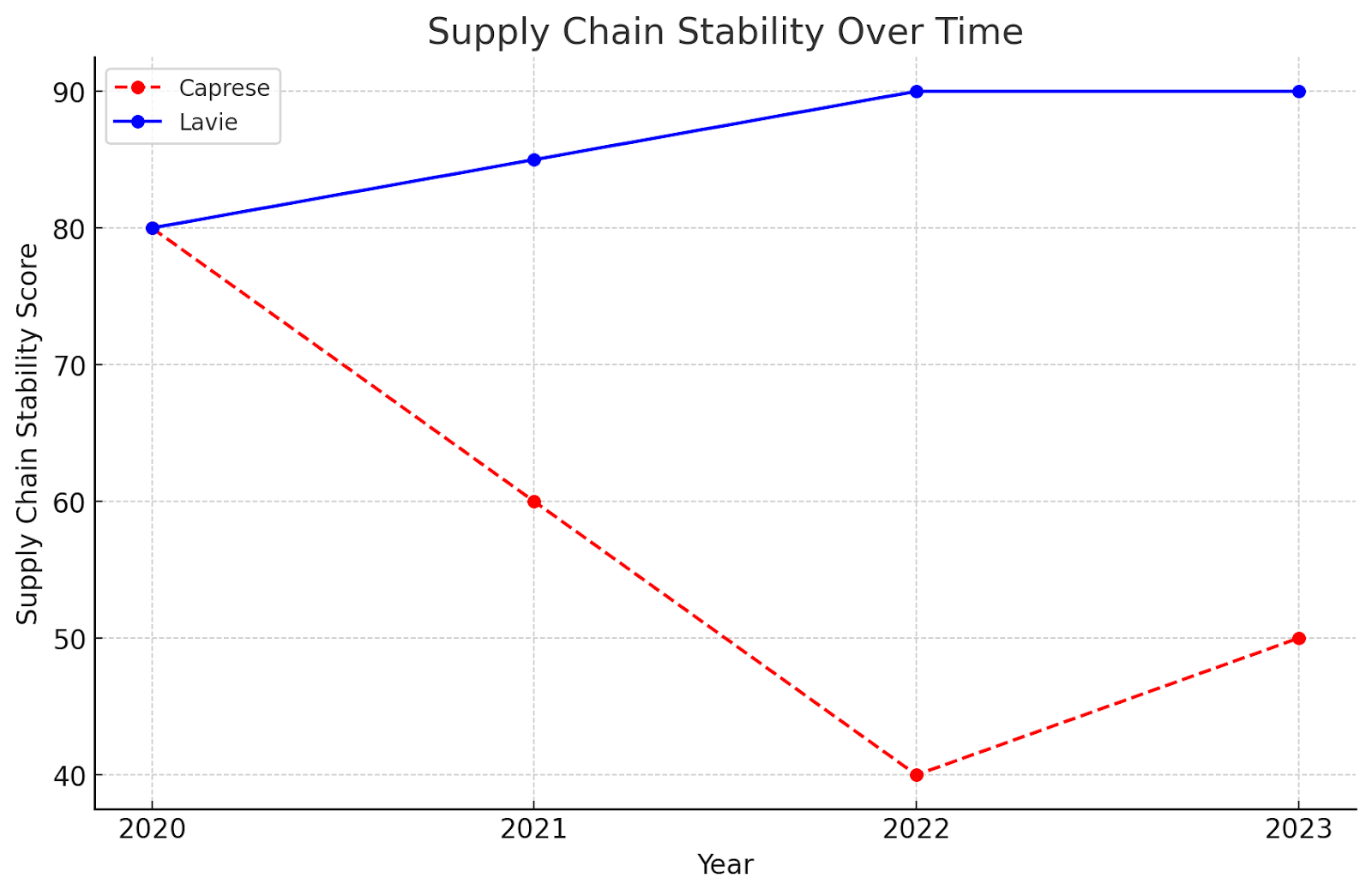

5. Supply Chain Dynamics: Fragility vs. Adaptation

The 2020–2022 global supply chain crisis served as a watershed moment. Caprese, heavily dependent on Chinese manufacturers, failed to reroute its supply chain rapidly, resulting in empty shelves and declining relevance. Lavie responded swiftly by localizing portions of its production, showcasing the benefits of agile supplier diversification.

Brand | Primary Supply Base | Adaptation Strategy | Outcome |

|---|---|---|---|

Caprese | China | No major pivot | Market share erosion |

Lavie | India + diversified | Rapid localization | Stable recovery |

This divergence in resilience maps directly to investor risk modeling. Brands with modular, regional supply chains and flexible production contracts offer reduced downside during geopolitical or macro disruptions.

Supply Chain Showdown – While Lavie’s stability steadily improved and held strong, Caprese struggled post-2020, with a steep decline highlighting the impact of disrupted imports and slower recovery.

Caprese vs. Lavie: Supply Chain Struggles – Caprese falters amid China lockdowns, while Lavie taps into its local adaptation toolbox, showcasing resilience through agile supply chain fixes.

Conclusion

The Indian handbag market represents a microcosm of India’s broader consumer evolution: a dual-speed economy where digital promise meets structural constraint. The next phase of growth will not be driven by digital adoption alone, but by distribution innovation, logistics sophistication, and brand differentiation. The winners will be those who stop treating handbags as mere fashion accessories—and start managing them like industrial assets.

The takeaway? Handbags might seem simple—but the business behind them is anything but. And that, dear reader, is why the handbag market is a lot more interesting than you might have thought